The pandemic ignites a food delivery war in France

Uber Eats, Deliveroo, Just Eat, Frichti, the names continue to ring off in the French food delivery market with each player on a mission to grab market share during a pandemic that has increased the digitalization of restaurants and the appetites of consumers.

In this battle creating loyalty has played the biggest role in swaying hungry customers and has seen it’s two biggest contenders launch their own heavily promoted free delivery subscriptions as a strategy to come out on top. However, regardless of the evident two-horse race, looking back at 2020 we can clearly see that the restaurant industries misfortune became food delivery’s boon for success across the board.

Uber Eats stays on top, but Deliveroo kicks into fifth gear

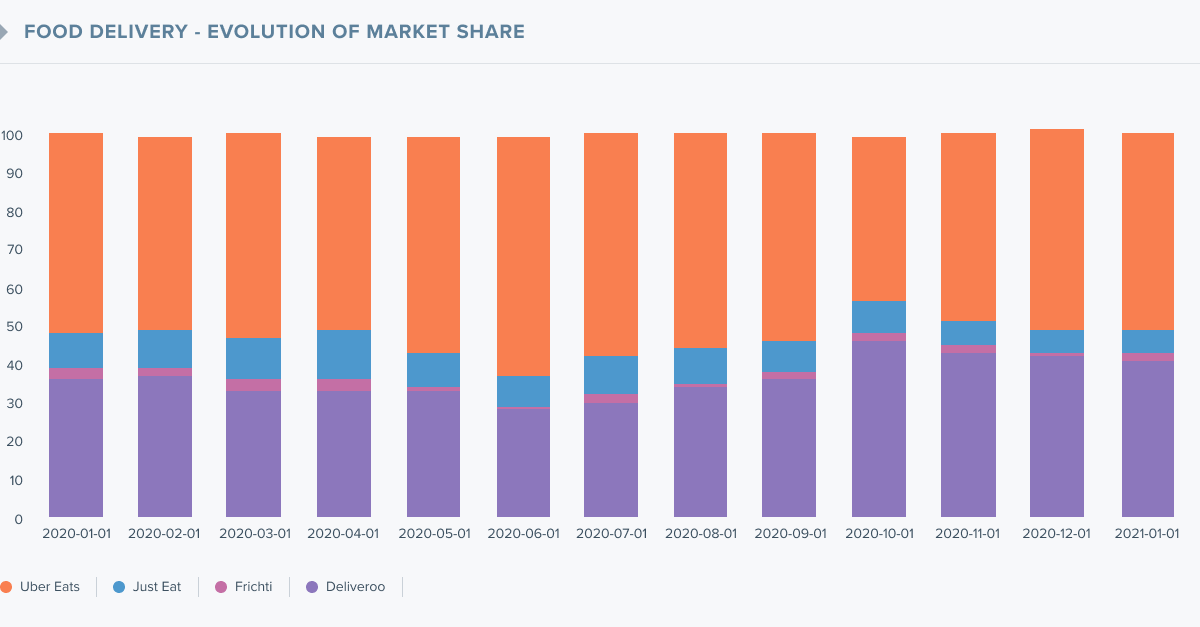

Starting off the year Uber Eats remained above the competition claiming a 52 per cent stake of the market, followed by Deliveroo with 36 per cent, Just Eat at 9 per cent and Frichti rounding out the bunch with 3 per cent of their own. This trend would continue until June when Uber Eats tightened its grip on the industry making up 62 per cent of the market, leaving only 28 per cent to their biggest competitor Deliveroo. The only unexpected shift in market share seen between January and June was the 13 per cent taken in by Just Eat in April which hasn’t been reached since.

However, as 2020 came to a long-awaited end, the race started to even out and saw Deliveroo start to close the gap going into 2021, taking 41 per cent of market share and gaining speed on the 51 per cent earned by Uber Eats in January. With the year starting on a high note for Deliveroo and Just Eat falling further down again with just 6 per cent of the industry, it marked a 12-month period of constant fluctuation between the players, which ended with the blue kangaroo taking a bigger piece of the delivery pie and Just Eat wanting more.

Deliveroo: The secret behind their latest jump

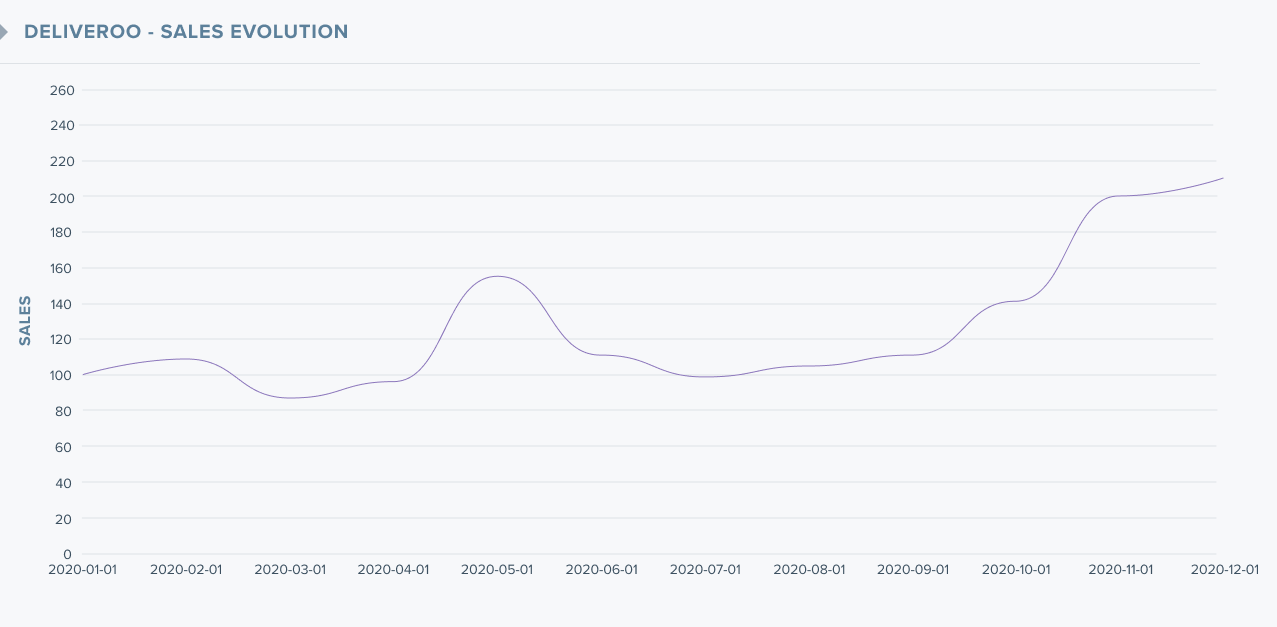

Just as the entire industry, Deliveroo, has enjoyed the circumstances of confinements and curfews that obliged restaurants to go digital and consumers to order in rather than take-out. To put things into perspective, the beginning of 2020 saw the platform announce their network of 12,000 restaurant partners, by the end of the year, the network grew to over 20,000. In the same time, their fleet of drivers grew from 11,000 to 14,000 to ensure the quality of their service.

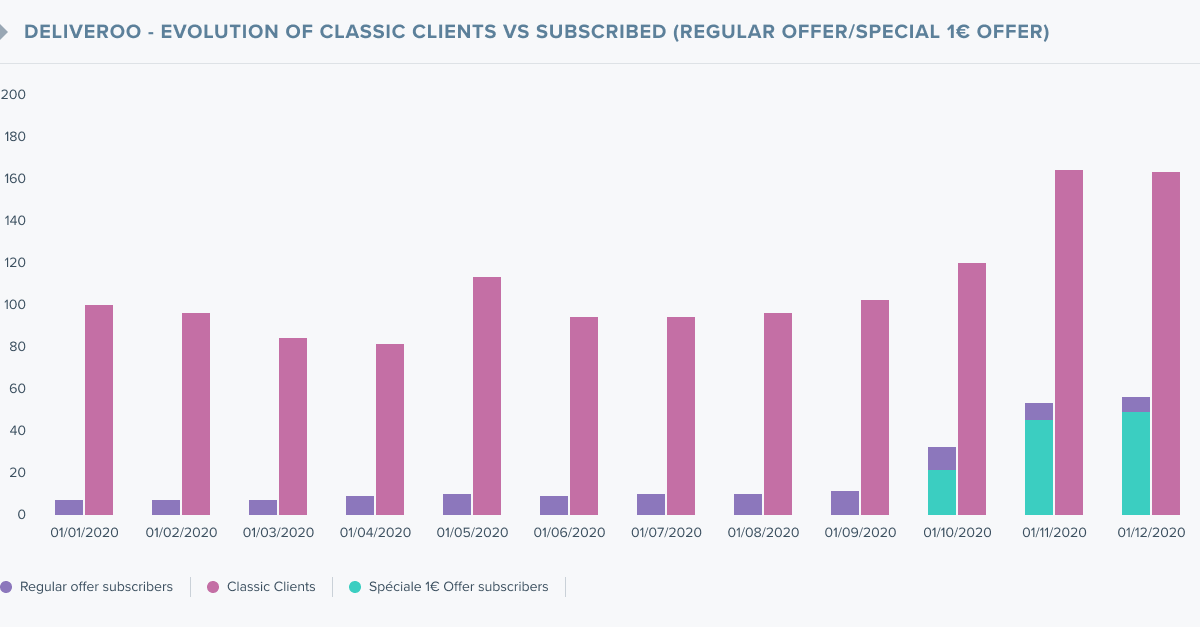

Despite the evident pandemic boost, what really made Deliveroo take-off in the fourth quarter of 2020 was the launch and promotion of their monthly Deliveroo Plus subscription. The offer brought unlimited free delivery to users for just a single euro per month until December 31st when the price rose to 5.99 euros. The result? October saw the number of subscribers multiply by three, a spectacular 27 per cent increase in sales, and a significant rise in new clients.

Cut to the launch of Uber Eats Pass: Same Subscription, Same effect

December saw Uber Eats launch their own unlimited free delivery pass with a similarly tempting promotion to make those with an appetite take the bait. The promotion surely contributed to the 14.75 per cent revenue increase seen between November and December 2020. What’s left to be seen for Uber Eats and Deliveroo is how many subscribers they will manage to retain now that the promotion is over.

Testing the limits of “whatever the cost”

The move to arms and subsequent jumps in activity from front-runners in the delivery race illustrates what’s up for the taking in a market that has seen a recent acceleration in user adoption. Nevertheless, the eye-watering promotions and cheap delivery too often come to the detriment of restaurants and the “neighbourhood hero” delivery people who continue to work harder for less. Signs of tension have seen challenger Just Eat take an ethical stand against the delivery powers that be and hire 4500 delivery people on permanent contracts in 2021. This concerted effort to build a responsible brand image and identity different from their counterparts could mean we are only at the beginning of a drawn-out struggle taken on by Just Eat to earn future market share.

Our Methodology

The data used in this article is based on the analysis of purchases made with the principal bank cards of consumers in France at the brands mentioned above in the period of 01/01/2020 to 22/01/2021. The data obtained for this study is anonymous and has been used with the express permission of consumers that have agreed to participate in the reward programs of our partners which includes banks, consumer fintechs, insurance companies and loyalty programs.