Embedded loyalty: Why banks will contextualize the loyalty experience

Loyalty is on the cusp of fully embedding itself into daily banking as financial institutions look to embed loyalty-driven services across bank touchpoints and payment cards.

Centered on contextualizing loyalty before, during, and after the purchase experience, embedded loyalty removes friction with a platform that ensures every aspect of loyalty happens seamlessly.

So why exactly are banks intent on contextualizing loyalty, and how will it create a frictionless experience for cardholders that brands and banks are eager to tap into?

All roads lead to loyalty

A convergence of market trends and the assets that banks hold make the embedding of loyalty not only an inevitability, but also a top priority for financial institutions adapting to the platform economy.

The banking services industry is grappling with a paradigm shift that has seen financial institutions that held all the keys to a market with no outside competitors deal with the reality of cross-industrial platformization. Non-financial organizations across industries now offer financial services and participate in ecosystems focused on embedding multiple services that personalize every experience to fulfill customer needs in a new way.

What’s on the line if banks don't act? A piece of a $20 trillion dollar opportunity that two-sided platforms are creating.

Loyalty will undoubtedly have a piece of that $20 trillion dollar pie. The industry is in the middle of three key players: consumers, merchants, and banks, and it is begging for a platform to unlock synergies between all three parties.

No doubt, due in part to the current inflationary context, consumer appetite for loyalty programs and promotions is at a high. 66% of respondents in a global study said that the ability to earn rewards influenced their spending habits. Furthermore, 84% noted they’re more likely to remain loyal to a brand with a loyalty program

Banks have no choice but to embrace the platform economy, and loyalty offers all the ingredients to be the next embedded experience.

Banks have all the ingredients (assets) to make it happen

Financial institutions have long held the trust of massive user bases, issued payment cards, and provided the primary touchpoint for financial management, making them an integral part of customers' lives. Still, the data they reserve access to is the main ingredient placing banks in a position to transform not just the loyalty industry but their structures, services, and revenue models to succeed in the future of banking.

As highlighted in Accenture’s Banking Marketplace report, the future of banking will depend on their ability to forge a "Market of One*" for every client, and banks stand out in this domain. Each bank customer possesses a distinct profile. Despite the categorization of their clientele, each customer's unique data, which remains largely siloed today, is unparalleled.

Banks possess the vital data to fashion "Markets of One" and have the capability to participate in platforms providing hyper-personalized experiences for each client.

However, the real measure of value is derived from the relevance, simplification, and efficacy of the provided services. To arrive at the “me banking” experience that helps clients arrive at specific outcomes, banks must fine-tune every specification to cater to each client's needs, whether delivering tailored payment methods or bank services. Given their assets and the boom of the platform economy, there's little stopping banks from leveraging their resources to deliver end-to-end experiences that present financial products in a contextual and personalized way. Thus facilitating both the everyday consumer life and the adoption of financial products that remain the main goal at the end of the day. Loyalty falls well within this scope, and banks will most likely take the baton from retailers in the future.

So what are banks missing?

Banks possess the core assets but need platforms to plug in third parties that provide contextual-based services to cardholders. Financial institutions must decide whether to take on the up-front costs of developing closed ecosystems or partner with platforms providing APIs and web apps that leverage their assets within a two-sided ecosystem that provides third-party offers.

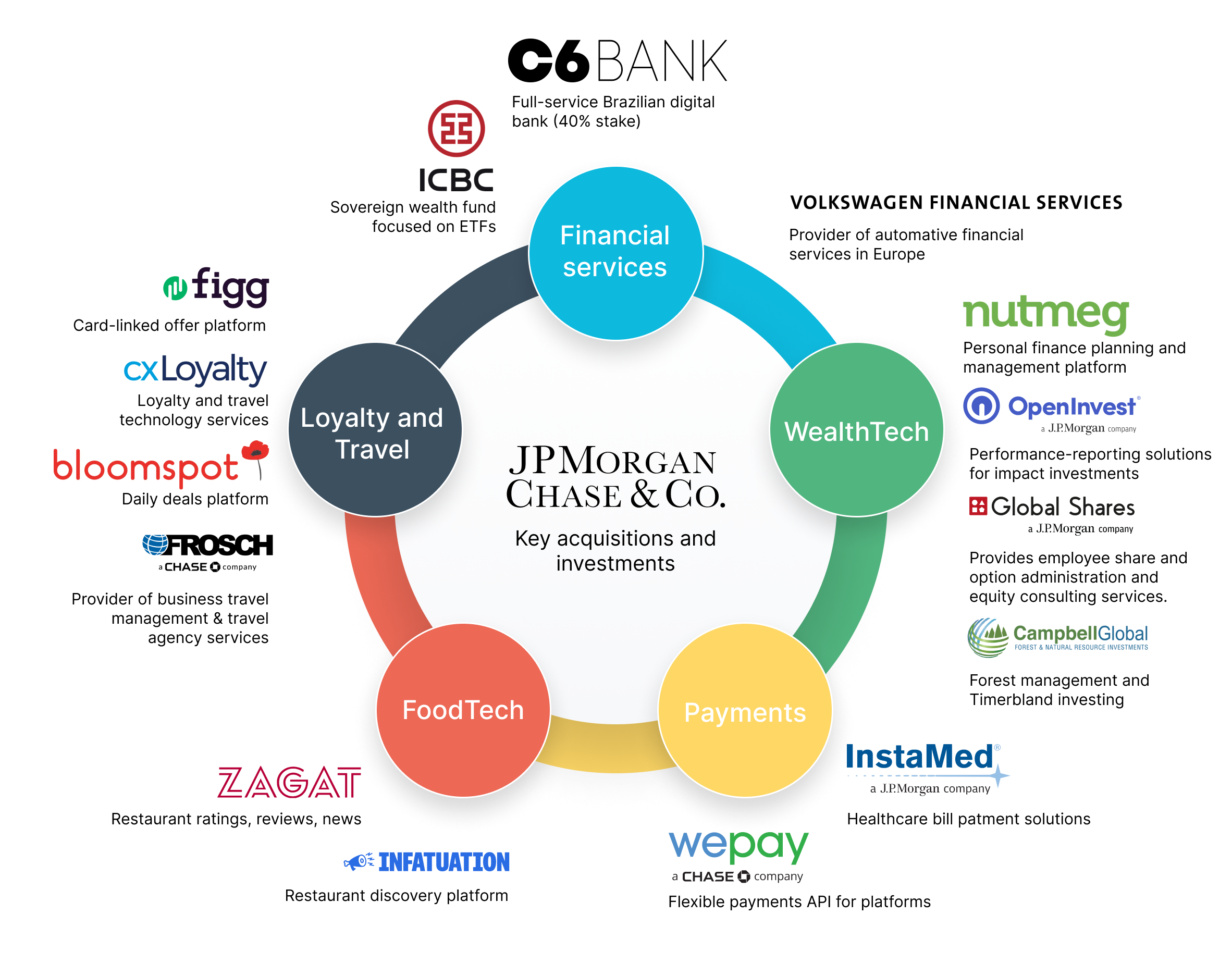

While some banks are making big moves, like JPMorgan Chase as seen in the image below, who acquired third parties within the travel space to create a closed ecosystem, other financial institutions enjoy the cost benefits and reduced time to market that open platforms provide.

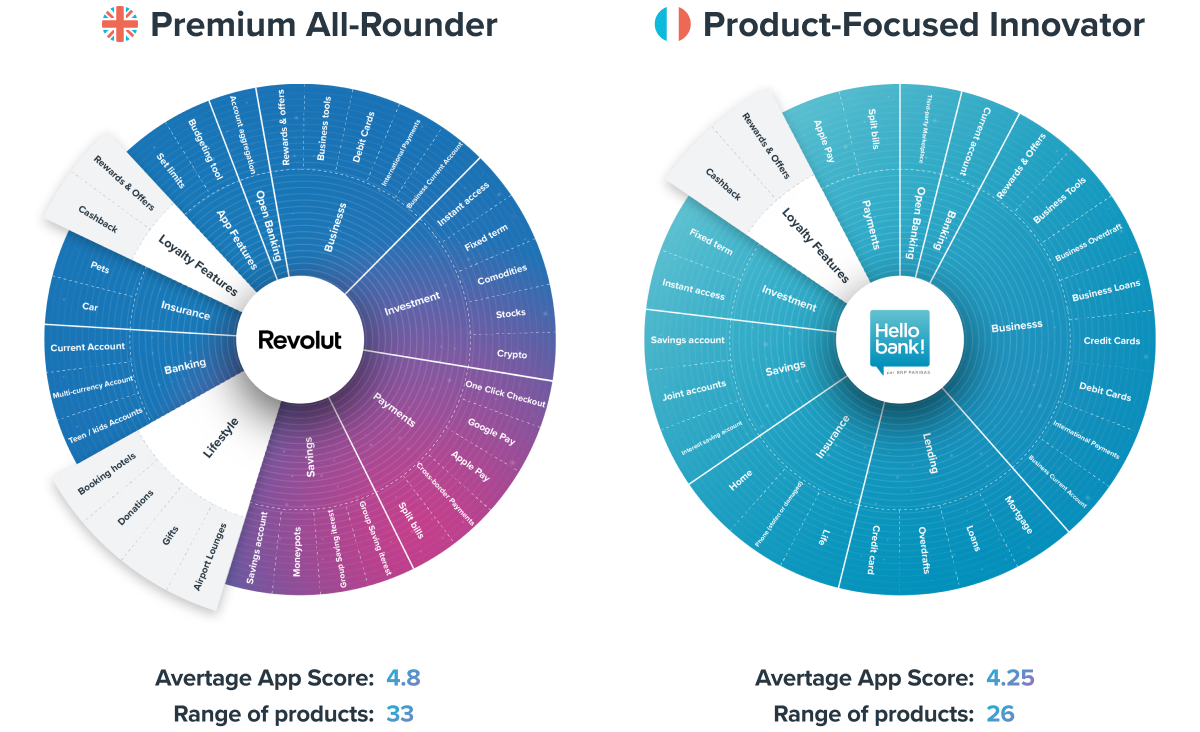

Aside from a few challenger banks such as Revolut who continues to broaden their shopping and loyalty offer, European banks are also falling behind Asian and North American counterparts in building super apps that embed financial products into lifestyle and loyalty experiences.

Rather than crafting services independently, EU banks should act quickly to collaborate with fintechs developing the platforms banks need to leverage their assets and create embedded experiences for a new customer-centric future.

Three ways banks will contextualize the loyalty experience

Seamless loyalty cards

By linking loyalty accounts to top-of-wallet payment cards, banks and merchants can remove the need to carry physical or digital copies.

Creating or linking a client's loyalty account with participating merchants would no longer involve giving out personal information to forms or retail employees. With embedded loyalty, a single prompt from your banking app asks a client to create or link a loyalty account to their payment card.

With the KYC verification of financial institutions and merchants of customers, the process would be instantaneous and completed in a single click. Think of one-click purchases on Amazon but for loyalty.

Creating a seamless point-earning experience gives cardholders another incentive to use a specific payment card and tightens their bond with banks, reducing their likeliness to churn. Competition between competing payment cards grows fiercer as new challenger banks and alternative options spoil consumers for choice. Card-linked loyalty presents another value-added service that could play a role in differentiating the value propositions of card issuers.

Amplifying the presence of brands in a space dedicated to loyalty.

Brand corners dedicated to loyalty and presence management within banking apps would be the natural extension of the bank statement. Imagine clicking a transaction on a bank statement and accessing a page devoted to a brand, in-app, that holds your loyalty card, points history, a place for your receipts, and a list of tailored offers.

Adding a brand corner solution provides bank clients with an extension of their loyalty programs to review their history across brands in a single place. It is also the ideal channel to display personalized product catalogs based on SKU-level purchase data that present customers with the most relevant items and promotions.

Available in a web app, integrating a white-label brand corner solution ensures that the features can be launched without overwhelming roadmaps. This aligns with the plug-and-play business model of platforms that allow banks and retailers to connect with consumers and ensure an exchange of value that benefits all parties in a short matter of time.

Enriching the payment experience with Automatic cashback

Merchants and banks want to simplify and enrich the shopping experience for clients willing to share pseudonymized data within an open platform. Automatic cashback enhances the payment experience for clients, incentivizes them to use their bank's debit or credit card, and is part of a crucial retention strategy for brands and financial institutions.

PayLead is one example of a technical layer bridging the gap between banks and merchants, bringing tangible rewards to European consumers. With over 30 banking partners across Europe, PayLead has developed and scaled a two-sided loyalty platform that facilitates data exchange between partners to increase the card usage of bank users and reward EU citizens for their purchase decisions.

PayLead’s partners have seen the results first-hand. Ma French Bank, the online bank of the La Banque Postale group, delivered on its mission to increase the purchasing power of its cardholders and saw a 9% increase in card usage and an 8% increase in overall spending among users earning automatic cashback.

Following the progress of a loyalty program launched by a leading financial institution in France, the numbers speak volumes about automatic cashback's ability to boost spending and card usage. Since launching their program, they've seen a 13% increase in average spending among rewarded active cardholders.

Increasing customer retention and engagement

Automatic rewards, loyalty hubs, and card-linked loyalty are all examples of embedded loyalty modules built to create the best experience possible by nearly making them invisible and placing them in the proper context.

These services not only increase the bank's presence in customers' daily lives but also increase the cost of churn by locking clients into an experience they can't find elsewhere. Being present throughout more experiences increases customer retention and engagement with their bank, whether directly within their touchpoints or indirectly through purchase journeys.

Bankin', the leading personal finance management application in France, has successfully leveraged loyalty modules to increase user retention and app engagement. After implementing an automatic cashback solution and purchase tab where users can find offers from participating brands, Bankin' improved retention of onboarded customers by +30 points. Looking at the engagement they've generated with automatic cashback, they leveraged the program by sending out communications regarding offers and saw a +211% rise in visits to their purchase tab in the app.

When looking at a large financial institution, we also see substantial jumps in engagement among customers who enjoy the loyalty experience of automatic cashback. After joining the program, users logged into the banking app or the bank's website 24% more times every month. Additionally, they were more likely to log in through different channels, with cashback users logging into the banking app and website 57% more times each month.

Building the future of embedded loyalty with PayLead

The world of embedded loyalty is set to see financial institutions enter the picture and provide their clients with a loyalty experience that differentiates their value proposition from their competitors and contextualizes their financial products.

PayLead's embedded loyalty platform gives banks the infrastructure to leverage their assets and instantly provide their clients with essential loyalty modules that seamlessly integrate into the banking applications of financial institutions.

With APIs and web-based applications, PayLead's solution streamlines the build process and helps banks launch faster, thus lowering the cost of entry, ensuring partnerships with leading retailers, and providing a best-in-class customer experience that over 30 banks across Europe have already chosen.

As banks and fintechs continue to involve themselves further in their customers' purchasing experience, we expect to see more players use embedded loyalty solutions as a strategic tool to increase engagement and boost card usage among cardholders.

Learn more about the results banks see from implementing a solution that serves their customers with contextual loyalty experiences Schedule a call